SEC Private Fund Adviser Reforms

· By Decile Group · Venture Legal

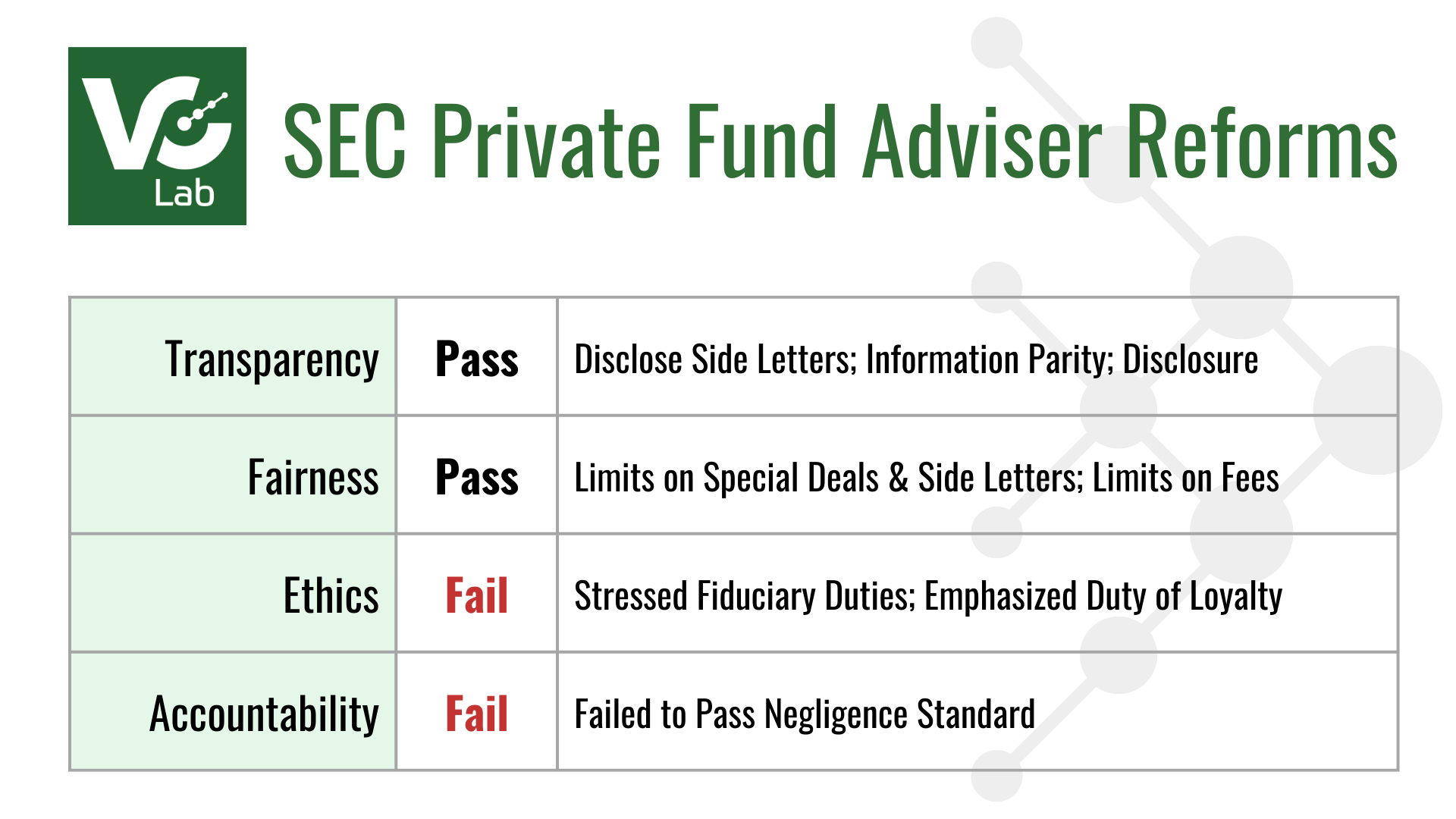

The United States Security and Exchange Commission (SEC) has updated its investment rules on Wednesday, August 23rd, 2023, targeting transparency, fairness, ethics, and accountability in private equity and venture capital. These changes aim to standardize practices within the industry, leading to varied feedback from venture capitalists, fund managers, limited partners, and other stakeholders.

VC Lab and Decile Group already comply with these new standards. Ethical organizations should always aim to exceed legal mandates, which generally set a low bar. Most VC Lab alumni funds are in alignment with these regulations, as well.

In contrast, many other firms and funds will need to make adjustments to their operations, from how they close Limited Partners to how they operate their fund governance. The full implications of the changes will take months to understand, as there is a lot of “gray area” in the new regulations.

A summary of the changes and the possible impacts of these changes are below.

SEC Transparency Measures (Passed)

The SEC passed sweeping transparency rules that affect the relationship between managers (referred to as advisers) and limited partners (referred to as investors).

Side Letters

Every Side Letter that provides preferential terms that may negatively impact other investors must now be shared with other Limited Partners. This measure ensures that all stakeholders are aware of any special provisions or agreements.

ISSUE: Big Limited Partners have demanded unfair Side Letters and VCs have offered sweetheart deals that will now all need to be disclosed.

EXAMPLE: A Side Letter may grant one Limited Partner the ability to review all Deal Memos before an investment is complete for compliance.

Information Sharing

Information made available to one Limited Partner (LP) should be equally accessible to all LPs. This rule ensures that no LP is given preferential treatment or undue advantage over others.

ISSUE: Some Limited Partners have participated in investment decisions and seen deals early to co-invest, which is not allowed with these changes.

Conflict Disclosure

The SEC now emphasizes that larger conflicts of interest should be approved by all Limited Partners, versus an Limited Partner Advisory Committee (LPAC). This aims at ensuring that LPs can make informed decisions.

SEC Fairness Measures (Passed)

The SEC passed watered down measures around fairness of the adviser and investor relationship based on commentary from many special interests.

Side Letter Restrictions

The extent to which special terms can be stipulated in Side Letters is now restricted. This ensures a level playing field for all investors.

Fee Restrictions

There are new limits on the types of fees venture funds can charge their investors. Additionally, certain financial transactions, such as borrowing by the adviser is prohibited without consent of the investors.

SEC Ethics Measures (Failed)

The SEC proposed not allowing advisers to remove their fiduciary duties, which did not pass because the SEC feels that the fiduciary duty rules are sufficient, and they reaffirmed which duties are most important.

Fiduciary Duties

The SEC reaffirmed the adequacy of existing fiduciary responsibilities. While the attempt to introduce new ethical standards did not pass, the agency stressed that certain fiduciary duties cannot be exculpated on a case by case basis.

Duty of Loyalty

Emphasis was placed on the importance of the duty of loyalty, underscoring its role in ethical investment practices.

SEC Accountability Measures (Failed)

The SEC proposed increasing the liability of advisers from gross negligence to negligence, which failed. This would have increased costs and decreased risk taking, according to the SEC.

Negligence Standards

There was an attempt to introduce a more stringent standard of negligence as opposed to gross negligence. This proposal, however, was rejected since it may lead to increased costs and lower risk taking.

New LPAC Rules and Guidance

The newly instated rules proposed alterations to the function and duties of Limited Partner Advisory Committees (LPAC).

Conflict of Interest

LPACs are now advised against voting on subjects where conflicts of interest are present.

Deal Information Access

There might be limitations on LPACs accessing deal-specific data before other LPs. This potential change, among others, can dramatically alter the role of LPACs.

New RIA Rules

For registered investment advisers (RIA), the SEC is mandating quarterly reports and audited annual financial statements. For areas of concern that pose conflicts of interest such as fee shifting to the investors, the SEC is forcing disclosure by all advisers of such conflicts. For more concerning areas such as the adviser borrowing from the fund or shifting expenses of a governmental investigation, the SEC now requires advisers to obtain consent from the investors. The SEC makes clear that disclosure and transparency is essential in order for investors to make informed decisions, and to level the playing field to avoid unfair outcomes for investors.

- Requires all SEC-registered advisers to provide investors with periodic information about private fund fees, expenses, and performance.

- Requires all SEC-registered advisers to cause each private fund to undergo an annual audit.

Note: Exempt Reporting Advisers are not subject to these rules.

Important: Normal funds will not be subject to a required audit.

Existing Fund Rules

Here is how the new SEC rules apply to existing funds, which includes the disclosure of Side Letters.

Exceptions

- Side Letter Amending: Existing Side Letters will not need to be amended.

- Redemption Provisions: Agreements that include preferential redemption terms are unaffected.

- Fund Borrowing: No changes to existing borrowing from a fund.

- Investigation Expenses: Funds can continue to charge for investigation-related expenses.

Not Exempt

- Side Letter Disclosure: Existing side letters must be disclosed to investors. The identity of the investor need not be disclosed.

- Fee Disclosures: Mandated disclosures for certain fees, clawback adjustments, and non-pro rata charges are now required.

Transition Period

- Funds below $1.5 billion in assets get 18 months to adapt to the changes.

Shifts in Venture Capital

The venture capital industry, being dynamic and fast-paced, will inevitably undergo shifts in response to these new SEC rules. Here’s a look at five possible changes:

Standardized Agreements

With the enforced transparency regarding Side Letters, venture firms may drift towards more standardized agreements to avoid complications and potential conflicts with Limited Partners.

Selective LP Onboarding

Funds might become more selective when taking on new Limited Partners, particularly those prone to demanding special terms, to simplify compliance.

LP Engagement

The enhanced transparency and fairness measures could lead to increased Limited Partner engagement and participation, especially in firms where LPs were previously passive or less involved.

Operational Overhauls

Funds that previously relied on special terms, fees, or specific financial transactions might have to revisit and overhaul their operational strategies to align with the new rules.

Increased Due Diligence

With the SEC’s emphasis on ethical standards and duty of loyalty, there might be an uptick in due diligence processes both before investments and during the course of partnerships.

Global Implications of SEC Changes

The ripple effect of the SEC’s alterations will likely extend beyond the borders of the United States. Given the stature and influence of the SEC, several international consequences are foreseeable:

Adoption by LPs Worldwide

While many Limited Partners (LPs) are U.S.-based, they often have a global investment footprint. As they adopt these SEC regulations, their international operations will inevitably be influenced.

Impact: Foreign venture funds seeking capital from U.S. LPs may find themselves needing to adhere to these guidelines to attract and maintain investment.

Regulatory Mimicry

The SEC, given its prominent role in financial regulation, often sets the tone for similar agencies around the world. It’s not uncommon for international regulatory bodies to borrow or adapt guidelines from the SEC to ensure synchronicity in global financial markets.

Impact: Countries looking to maintain a competitive edge in attracting international capital may quickly introduce similar rules, leading to a more homogenized global venture capital landscape.

Standardization of VC Practices

As U.S. venture capital firms adapt to these rules, their international branches or affiliated funds might adopt similar practices for the sake of uniformity.

Impact: This could result in a global shift towards more transparent and standardized venture capital operations.

Increased Scrutiny on Ethics

With the SEC emphasizing ethical behaviors, there could be a global push towards prioritizing ethical investment practices, even in regions where such standards were previously lax.

Impact: This could lead to a global emphasis on ethics in investment, potentially influencing sectors beyond venture capital.

In essence, while the SEC’s primary jurisdiction is the United States, its influence, coupled with the global nature of finance, means these changes could reshape venture capital practices worldwide. As firms, LPs, and other stakeholders adjust, the broader international investment community will likely take note, adapt, and evolve.

A Hypothetical Case

The implications of the new SEC rules can be better understood by examining the hypothetical case of Example Capital, a venture fund with a rich history of crafting diverse Side Letters for different Limited Partners.

Historically, Example Capital engaged in practices such as:

- Granting specific LPs preferential terms in Side Letters

- Allowing particular LPs exclusive rights to co-invest in specific deals

Challenges

Side Letter Disclosures

Example Capital, with its numerous custom-tailored Side Letters, faces the challenge of disclosing these to new LPs post-compliance.

Example: A Side Letter with Alpha Investors, a major LP in Example Capital, might have granted them reduced management fees. Sharing such economic terms could lead to unrest among other LPs or new potential partners who might demand similar terms.

Co-investment Equalization

Example Capital allowed certain LPs to co-invest on privileged deals. With the new regulations, such practices could be viewed as offering undue advantage.

- Example: If Gamma Group, another LP, discovered that Alpha Investors had early access to a lucrative deal they missed out on, it could raise concerns of fairness and equal opportunity.

Solutions

Open Communication Channels

To address potential unrest among LPs regarding disclosed economic terms, Example Capital might initiate an open dialogue with its LPs, explaining the historical context of such agreements and assuring them of the fund’s commitment to fairness moving forward.

Transparent Co-investment Opportunities

Example Capital can introduce a structured co-investment procedure. Any opportunity presented to one LP must be available to all, ensuring a level playing field.

Standardizing Side Letters

Example Capital could move towards crafting standardized Side Letters, minimizing special terms and conditions. While this might lead to losing some LPs, it ensures smooth operation under the new regulations.

Re-evaluating LP Onboarding

Example Capital could reconsider their LP onboarding process, becoming selective about Limited Partners that demand Side Letters.

Example Capital’s challenges, while hypothetical, underline the complex scenarios many funds could face with the new SEC regulations. Addressing these requires both strategic adjustments and proactive communication.

Conclusion

The new SEC rules aim to provide greater transparency, fairness, and ethics in the venture capital sector. As the industry navigates these changes, it remains to be seen how these rules will reshape the future of investments.

- Legal Support